How to Avoid Overoptimization in MT4 EAs: Proven Strategies for Reliable Trading

How to avoid overoptimization in MT4 EAs is a critical topic for traders who want Expert Advisors that work consistently—not just in backtests. Overoptimization, often called curve-fitting, leads to trading robots that look amazing on historical charts but fall apart the moment they encounter real market conditions. This article breaks down practical steps, proven methods, and expert-level insights to help you build or select MT4 EAs that can survive unpredictable market environments.

Understanding Overoptimization in MT4 EAs

Overoptimization happens when a trading system is trained too closely on past market data. Instead of identifying robust trading logic, the EA adapts to random noise, producing backtest results that appear perfect but are unreliable in live trading.

A curve-fitted EA often shows unusually high win rates, extremely smooth equity curves, or profit factors that look too good to be true. While these results may impress new traders, experienced developers know that such outcomes often signal unstable, fragile strategies.

Key Characteristics of Overoptimized Expert Advisors

- Too many adjustable parameters

- Unrealistically high profit factor (3.0+)

- No losing months in backtests

- Sharp equity curve with almost no drawdowns

- Sensitivity to small parameter changes

These warning signs indicate that the EA might collapse when market conditions shift even slightly.

Why Overoptimization Weakens Trading Performance

Because the EA is tuned to historical noise, it fails to adapt to new price behavior. Markets evolve—volatility shifts, spreads widen, and liquidity conditions change. An overoptimized system cannot handle these fluctuations, leading to poor live results.

Causes of Overoptimization in MT4 EA Development

Several behaviors and development choices lead directly to overfitted trading robots.

Excessive Parameter Fitting

When traders adjust dozens of variables—stop-loss, take-profit, moving averages, filters—the system stops being logical and starts being customized to specific price sequences.

Limited Historical Data Use

Using only a short historical period hides the full range of market conditions. Optimization over a narrow timeframe encourages curve-fitting.

Ignoring Forward Testing Requirements

Without forward testing, developers rely solely on backtests, which do not reflect real market variations like spread changes, slippage, or volatility spikes.

How to Avoid Overoptimization in MT4 EAs

This section explains the most important techniques for ensuring your MT4 EA is truly robust.

Use Sufficient Quality Historical Data

A strong EA must be tested across multiple years—including periods of high volatility, low volatility, trending markets, and sideways markets.

Ensuring Data Accuracy and Tick Quality

Aim for 90–99% modeling quality using reliable data sources. This reduces the risk of misleading results caused by inaccurate price feeds.

Apply Robust Walk-Forward Testing

Walk-forward testing validates how well an EA performs on new, unseen data.

In-Sample vs Out-of-Sample Testing

- In-sample data is used to optimize strategy parameters.

- Out-of-sample data tests whether the strategy maintains performance outside the optimized window.

A healthy EA performs well across both datasets.

Limit the Number of Optimized Inputs

The more parameters an EA has, the higher its susceptibility to overoptimization. A strong strategy should work with as few adjustable inputs as possible.

The Principle of Parsimony in Trading Systems

Also known as Occam’s Razor, this principle states:

The simplest model that performs well is usually the most reliable.

Run Stress Tests and Monte Carlo Simulations

Monte Carlo analysis adds randomness to trades, spreads, and execution to determine whether an EA is truly stable. If small changes cause dramatic shifts in results, the EA is overoptimized.

Best Practices for Real-World EA Deployment

Avoid Overleveraging and Unrealistic Strategy Expectations

Even the best EA will experience losing periods. Overleveraging magnifies losses and increases the risk of blowing an account.

Monitor Live Performance vs Backtest Performance

A healthy EA should show similar behavior in live trading, even if the exact profits vary. Large discrepancies indicate poor robustness.

Tools and MT4 Features to Prevent Overoptimization

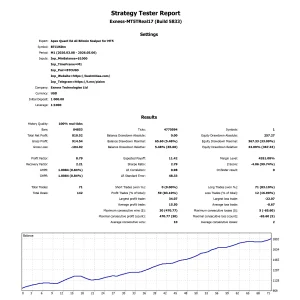

MT4 Strategy Tester Tips

- Use “Every Tick” mode

- Record modeling quality

- Run optimizations over long periods

Third-Party Tools for Robust EA Validation

Tools like QuantAnalyzer or Tickstory help validate EA performance using high-quality tick data.

Common Mistakes Traders Make When Optimizing EAs

Ignoring Market Regimes

Markets shift between trending and ranging conditions. Optimizing for only one regime results in unstable strategies.

Optimizing for High Profit Factor Only

A high profit factor is meaningless if drawdowns or consistency metrics are unrealistic.

FAQs About How to Avoid Overoptimization in MT4 EAs

1. What is the fastest way to detect overoptimization?

If small parameter changes drastically alter results, the EA is likely overoptimized.

2. How much historical data is enough?

At least 5–10 years for major forex pairs and more for volatile assets.

3. Should I optimize all EA parameters?

No. Optimize only the most essential ones and keep others fixed.

4. Does walk-forward testing guarantee success?

Not a guarantee, but it greatly improves reliability.

5. Can free MT4 EAs avoid overoptimization?

Some can, but many free EAs are heavily curve-fitted.

6. Do Monte Carlo simulations matter?

Yes. They provide realistic expectations of performance fluctuations.

Conclusion

Learning how to avoid overoptimization in MT4 EAs is one of the most valuable skills in algorithmic trading. By focusing on robust testing methods, limiting parameters, using high-quality data, and applying walk-forward validation, traders can build reliable Expert Advisors that survive real market conditions—not just historical tests.

Most Popular Forex EA

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

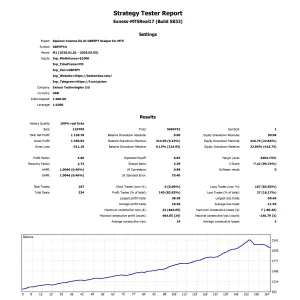

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

324 in stock

Original price was: $1,861.99.$187.99Current price is: $187.99.

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

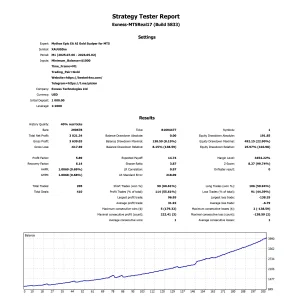

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

47 in stock

$0.00 $797.99Price range: $0.00 through $797.99

Powerful Forex VPS for MT4 & MT5 – Best Price

182 in stock

$44.99 $359.99Price range: $44.99 through $359.99

Top 2000 Trading Tools for Forex Success (EA & Indicator)

In stock

Original price was: $9,999.99.$0.00Current price is: $0.00.

Zenith Matrix XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $899.99Price range: $0.00 through $899.99 Gold Forex EA

Gold Forex EA