Backtest MT4 EAs on Tick Data: 10 Expert Tips

Backtesting plays a huge role in determining whether an Expert Advisor (EA) can stand up to real market conditions. When traders rely on MT4’s default data, results often appear “too perfect” because the system uses interpolated price movements rather than real ticks. That’s why using tips for backtesting MT4 EAs on tick data becomes essential if you want reliable, real-world performance insights.

In this guide, you’ll learn exactly how to prepare MT4, choose the right tick data sources, configure your backtest correctly, and validate results like a professional EA developer.

Understanding Tick Data in MT4

Tick data represents every tiny price movement that occurs in the market. Instead of only capturing candles at fixed intervals, tick data tracks micro-fluctuations that automated strategies often rely on.

What Makes Tick Data Different From Standard Data?

Standard MT4 data uses OHLC values and artificially fills the gaps between candle highs and lows. This creates unrealistic market movement, especially for:

- Scalping EAs

- Grid systems

- Martingale strategies

- High-frequency algorithms

- News-based strategies

Tick data removes guesswork by mirroring actual market behavior.

Why EA Developers Prefer Precision Tick Data

Tick-based simulation offers:

- Accurate spread modeling

- True slippage events

- More reliable stop-loss and take-profit triggers

- Realistic latency and execution effects

This makes your backtest a better reflection of how your EA performs in the real world.

Preparing MT4 for High-Quality Tick Data Backtesting

Before learning the best tips for backtesting MT4 EAs on tick data, your platform must be set up correctly.

Choosing a Reliable Tick Data Source

Trusted tick data providers include:

- Dukascopy (most popular)

- TrueFX

- Darwinex (premium quality)

- Custom proprietary feeds

Your chosen provider should offer:

- Full historical range

- Millisecond-accurate timestamps

- Low-latency recording

Higher quality data equals better EA evaluation.

Installing and Configuring Tick Data Suite (TDS)

Tick Data Suite (TDS) is one of the best tools for MT4 backtesting. It provides:

- 99.9% modeling quality

- Adjustable spread and slippage

- Variable execution latency

- Real tick volatility simulation

- Spread history emulation

With TDS installed, your backtest becomes nearly identical to a real market environment.

Setting Up Proper Spreads, Slippage & Commission

To avoid misleading results, configure:

- Commission per lot (make sure it matches your broker)

- Variable spread settings

- Slippage profiles

- Trading hours specific to your broker

Backtests often fail because spreads are unrealistically tight or costs aren’t included.

Top Tips for Backtesting MT4 EAs on Tick Data

Below are the most effective and practical tips for backtesting MT4 EAs on tick data that professional algo traders use.

Tip #1 — Use 99.9% Modeling Quality for Realistic Results

Without 99.9% modeling quality, your EA could pass the backtest but fail instantly in live trading. Tick data and TDS ensure every trade trigger is based on real market behavior.

Tip #2 — Optimize Only After Stability Testing

Never jump straight into optimization. Start by evaluating your EA on:

- Unoptimized default settings

- Multiple timeframes

- Various market conditions

Only optimize once you confirm the EA is stable.

Tip #3 — Test on Multiple Market Conditions

Evaluate your EA across:

- Trending periods

- Sideways markets

- High-volatility news spots

- Low-liquidity zones

This prevents curve-fitting and gives you a well-rounded performance picture.

Tip #4 — Use Variable Spread Instead of Fixed Spread

Real markets don’t operate on fixed spreads. Spreads change constantly due to:

- Volatility

- Liquidity shifts

- Economic releases

Variable spreads reveal vulnerabilities most backtests hide.

Tip #5 — Analyze Trade Logs to Detect Strategy Weaknesses

Your trade log shows:

- Execution delays

- Missed orders

- Spread-sensitive behavior

- Stop-loss premature triggers

These insights help you refine your EA with precision.

Tip #6 — Run Monte Carlo Simulations for Robustness

Monte Carlo testing introduces randomness to:

- Order execution

- Spread variation

- Slippage

- Price paths

This shows how durable your EA is under unpredictable real-world scenarios.

Tip #7 — Verify Broker Execution Parameters

Some brokers enforce rules like:

- Stop level distances

- FIFO execution

- Market execution slippage

Your EA must comply with these constraints during backtests.

Avoiding Common Backtesting Mistakes in MT4

Even experienced traders run into these issues.

Data Gaps and Incorrect Time Zones

Inconsistent data can cause:

- Gaps between candles

- Long bars

- Missing ticks

- Incorrect volatility measurements

Always synchronize your tick data time zone with your broker.

Wrong Modeling Settings and Inaccurate Parameters

Ensure that:

- Your EA’s parameters match your broker’s specs

- Commission and spreads are correctly applied

- The test starts and ends at logical periods

Details matter when testing tick-sensitive strategies.

Validating Your EA After the Backtest

A good backtest isn’t the end of the journey—it’s the beginning.

Demo Testing and Real Account Micro-Validation

Run your EA on:

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99| Validity | Monthly, Quarterly, Semi Annually, Annually |

|---|

- A demo account

- A cent account

- A micro real account

This gives you live-market confirmation with minimal risk.

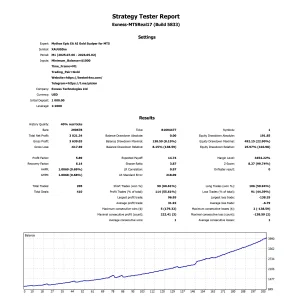

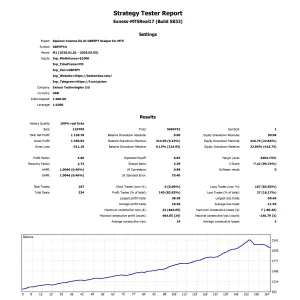

Key Metrics to Validate (RR, PF, Drawdown, Stability)

Check:

- Profit Factor (PF)

- Sharpe ratio

- Max drawdown

- Consecutive losses

- Equity curve smoothness

Consistency matters more than total profit.

FAQs About tips for backtesting mt4 eas on tick data

1. Why is tick data better for MT4 backtesting?

Tick data provides realistic price movement and avoids interpolation errors found in standard MT4 data.

2. Do I need Tick Data Suite to get 99.9% modeling quality?

Yes, MT4 alone cannot achieve 99.9% modeling quality without external tools.

3. How far back should I backtest an EA?

At least 5–10 years, depending on strategy type.

4. Can fixed spreads ruin a backtest?

Yes, they hide slippage and volatility effects, especially for scalping EAs.

5. What is the minimum tick quality I should use?

Always aim for 99.9% modeling quality.

6. Should I optimize before or after robustness testing?

Always after robustness testing to avoid curve-fitting.

Conclusion

Mastering these tips for backtesting MT4 EAs on tick data will dramatically improve the reliability of your strategy evaluations. Tick-accurate backtesting isn’t just technical—it’s essential for building confidence in your EA before risking real money.

Using proper data, realistic market conditions, and strong validation techniques can elevate your results from “theoretical” to practically useful. If you want to explore more independent resources, platforms like Investopedia offer helpful articles on algorithmic trading fundamentals.

Most Popular Forex EA

Onix Stratos XAUUSD EA: AI Smart Scalper for MT5

In stock

$0.00 $999.99Price range: $0.00 through $999.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $399.99Price range: $0.00 through $399.99

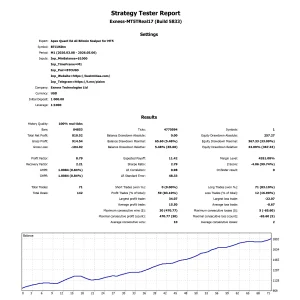

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

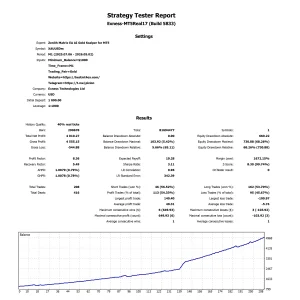

Zenith Matrix XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $899.99Price range: $0.00 through $899.99

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

In stock

$0.00 $797.99Price range: $0.00 through $797.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

In stock

Original price was: $109.99.$87.99Current price is: $87.99.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99

Gold Forex EA

Gold Forex EA