How to Backtest MT4 EA with Tick Data: 9 Powerful Steps for Accurate Results

Understanding MT4 Backtesting and Why Tick Data Matters

When you’re trying to automate a trading strategy, you don’t want to risk real money before you know how it might have behaved in the past. That’s where MT4 backtesting comes in. It lets you run your Expert Advisor (EA) over historical prices and see hypothetical trades, equity curves, and risk metrics.

But here’s the catch: the quality of your backtest is only as good as the quality of your data. Most traders start with default broker history, which often uses only bar data and approximated ticks. That can make a strategy look far better (or worse) than it really is.

What MT4 backtesting actually does under the hood

The MT4 Strategy Tester replays historical data bar by bar and generates artificial “ticks” between the Open, High, Low, and Close of each candle. Depending on the mode you choose (Open prices only, Control points, Every tick), MT4 makes assumptions about how prices moved inside each candle.

Key points:

- MT4 uses .hst files to store chart history and .fxt files for backtesting.

- In “Every tick” mode with normal broker data, MT4 does not use real ticks; it simulates them between OHLC values.

- For EAs that depend on intra-bar behavior (scalpers, grid, martingale, trailing stops, etc.), this simulation can drastically change the results.

So, if your EA opens and closes trades within a few pips, you need more precision than bar-only approximations.

The difference between bar data and tick data

- Bar data: Open, High, Low, Close for each timeframe candle. Good for high-level strategies that act only at bar open.

- Tick data: Every price change recorded by the broker or data provider. This gives you the exact sequence of price moves inside each bar.

Benefits of real tick data:

- More accurate modelling of stop losses, take profits, and trailing stops.

- Better spread and slippage simulation.

- More realistic results for scalping, high-frequency, and intraday systems.

Why most “Every tick” tests in MT4 are misleading without real ticks

Many traders assume that selecting “Every tick” in the Strategy Tester automatically means “accurate tick-data testing.” Unfortunately, that’s not true by default. Without imported tick data and a proper .fxt file, MT4 simply builds pseudo-ticks from bar data.

That often leads to:

- Unrealistic order fills.

- Ignored spread spikes.

- Incorrect stop-loss or take-profit hits.

Using real tick data, or a reliable tick generator based on high-quality one-minute data, significantly improves the reliability of your results.

Preparing Your MT4 Platform for Professional Tick-Data Backtests

Before you dive into the full step-by-step guide, you want a clean MT4 environment that’s dedicated to testing. Mixing your live trading terminal with heavy backtesting can slow everything down and clutter your history.

Choosing a reliable tick data source (Dukascopy, brokers, and more)

Popular sources of tick data include:

- Data derived from Dukascopy price feeds (used by many third-party tools).

- Some brokers provide downloadable historical tick data for their instruments.

- Paid data vendors offering cleaned and normalized tick histories.

When choosing a provider, pay attention to:

- Coverage (symbols and years available).

- Data cleanliness (few gaps or obvious spikes).

- Time zone settings (important for matching broker server time and sessions).

An external resource like the MetaQuotes or data tool documentation is helpful if you want exact import formats and file structures. For example, you can check the official MetaTrader 4 documentation site for file details and Strategy Tester behavior.

Selecting the right symbol, timeframe, and date range

Decide upfront:

- The symbol (e.g., EURUSD, GBPUSD, XAUUSD).

- The timeframes your EA will trade (e.g., M1, M15, H1).

- The date range you want to test (e.g., last 5–10 years if available).

Longer histories give you a more robust view, but they also increase:

- Import time.

- Disk usage.

- Backtest duration.

A practical approach is:

- Use at least 3–5 years of data for initial robustness checks.

- Extend to longer periods if your EA performs well and isn’t clearly over-fitted.

Disk space, performance, and data management basics

Tick data is heavier than bar data. For a single symbol over many years, you may need:

- Several gigabytes of disk space.

- Patience for data download and conversion.

Tips:

- Use a SSD for faster read/write.

- Keep a separate MT4 directory just for backtests.

- Regularly clean old .fxt and .hst files if you’re not using them anymore.

Step-by-Step Guide: how to backtest mt4 ea with tick data

This is the heart of the process. Follow these steps and you’ll be running realistic tick-data backtests in MT4 with far more confidence.

Step 1: Install MT4 and create a dedicated testing terminal

- Download MT4 from your broker or a trusted source.

- Install it to a separate folder (e.g.,

C:\MT4_Backtest\). - Disable auto-updates if you rely on specific testing tools that need a stable build.

- Log in with a demo account (no need for live credentials).

Having a dedicated terminal avoids conflicts with live trading and keeps your data folder clean.

Step 2: Downloading and converting tick data

Depending on the tool you choose, the exact clicks differ, but the core idea is:

- Select your symbol and date range in the data tool.

- Download raw tick data (or high-resolution M1 data that can be converted to pseudo-ticks).

- Convert this data into a format MT4 understands (commonly through:

- Direct .hst generation for the chosen symbol/timeframe.

- Creation of an .fxt file for the Strategy Tester).

Many tick-data utilities let you also set:

- The spread you want to use (fixed or variable).

- Whether to include commission and swap into the backtest.

Step 3: Importing tick data into MT4’s History Center

Inside MT4:

- Press F2 to open the History Center.

- Pick your symbol (e.g., EURUSD) from the list.

- Select the timeframe (usually M1) if you’re using M1-based tick generation.

- Click Import, then choose the CSV or file generated by your tick-data tool.

- Confirm the time format, separator, and decimal places.

- Click OK and let MT4 load the data.

After import:

- Open a chart for that symbol and timeframe.

- Scroll back to verify that history is filled as expected.

Step 4: Setting up your EA inputs and test model in Strategy Tester

Open the Strategy Tester (Ctrl+R):

- Choose your Expert Advisor in the “Expert Advisor” dropdown.

- Set the Symbol and Period.

- Choose Model:

- For tick tests, use “Every tick” (or the specific mode recommended by your tick-data tool).

- Set your Spread:

- You can use a fixed number (e.g., 10 = 1.0 pip on 5-digit accounts) or “Current” (not ideal for historical tests).

- Under Expert properties:

- Set your Initial deposit, Currency, and Leverage.

- Tune the EA’s input parameters (lots, stop loss, TP, filters, etc.).

Make sure the date range in the Strategy Tester matches the period where you actually imported tick data.

Step 5: Running the first test and checking the modelling quality

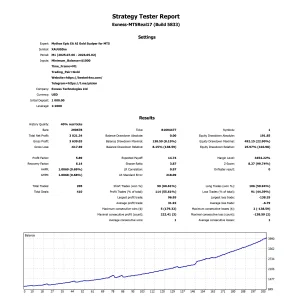

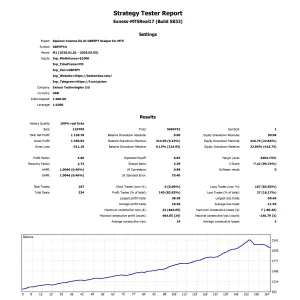

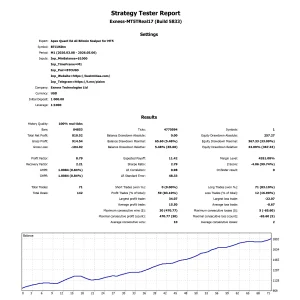

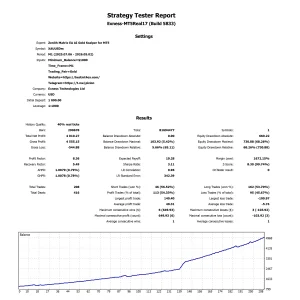

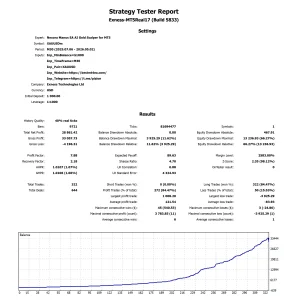

Click Start and let MT4 run the backtest. When it’s done:

- Switch to the Results tab to see trade-by-trade details.

- Check the Graph tab to see the equity curve.

- Look at the Report tab for:

- Modelling quality (% – often 90% for high-quality M1-based tests; some tools hack this to show 99% when using real tick data).

- Total net profit.

- Drawdown (absolute, maximal, and relative).

- Profit factor and expected payoff.

If your modelling quality is very low, or you see “mismatched chart errors” in the Journal, it usually means:

- Your history doesn’t fully cover the test period.

- Time zone or symbol naming doesn’t match between data and MT4.

Step 6: Interpreting key backtest metrics (profit factor, drawdown, etc.)

Don’t just look at net profit. Important metrics include:

- Profit factor: Gross profit / gross loss. Above 1.5 is usually considered decent; above 2 is strong (but not a guarantee).

- Maximal drawdown: Largest equity drop in money terms.

- Relative drawdown: Largest equity drop as a percentage of your balance/equity.

- Win rate & payoff ratio: High win rate alone is meaningless if losses are huge.

Ask yourself:

- Is the equity curve relatively smooth?

- Does the strategy survive major market events in the data (crashes, spikes, news)?

- Are results consistent across different time periods?

Step 7: Fixing common issues (mismatched charts, gaps, errors)

Common problems and quick fixes:

- Mismatched chart errors: Re-import history, ensure you have continuous data for the whole period.

- Strange spikes or flatlines: Data may be corrupted; re-download or try another source.

- “Off quotes” or trade context errors: Often EA logic issues rather than data problems; check order handling, magic numbers, and trade filters.

Once you’ve cleaned up these issues, repeat your backtest until the log is relatively free of data-related warnings.

Advanced Tick-Data Techniques for MT4 EA Developers

Using variable spreads, commissions, and slippage

Real markets don’t have a fixed spread. To make tests closer to reality:

- Use tools that allow variable spread based on historical data.

- Add realistic commission per lot if your broker charges it.

- Simulate slippage (positive and negative) on each order.

This reduces the risk that your EA only works in a perfect, friction-free environment.

Handling news spikes and volatile sessions in tick backtesting

News events and session opens can cause:

- Large spikes.

- Rapid spread widening.

- Slippage.

If your tick data includes these events, you’ll see how your EA behaves in truly stressed conditions. You can:

- Add filters that avoid trading during high-impact news.

- Tighten risk settings around session opens/rollovers.

Portfolio and multi-pair EA testing with tick data

Some EAs trade multiple symbols. You can:

- Backtest each symbol separately with its own tick data.

- Analyze correlations: does the EA lose on all pairs at the same time?

In MT4, native multi-symbol backtesting is limited, but you can still get a good picture by combining results and tracking total equity manually or with additional tools.

Best Practices to Avoid Overfitting Your MT4 EA

In-sample vs out-of-sample testing with tick data

To avoid “curve fitting” your EA to past data:

- Split your data into in-sample (for optimization) and out-of-sample (for validation).

- Optimize parameters only on the in-sample period.

- Run a fresh backtest on out-of-sample data using the chosen parameters.

If performance collapses in out-of-sample testing, your strategy might be overfitted.

Walk-forward analysis and robustness checks

A more advanced approach is walk-forward testing:

- Optimize on a time window (e.g., 1 year).

- Test the optimized parameters on the next period (e.g., next 6 months).

- Slide the window forward and repeat.

If the EA behaves reasonably well across many walk-forward passes, it’s likely more robust.

Monte Carlo simulations and other stress tests

Some tools allow you to:

- Randomize trade order.

- Randomize slippage and spreads.

- Add small noise to entry/exit prices.

If your EA still survives and performs reasonably under such randomization, that’s a strong sign it’s not fragile.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99| Validity | Monthly, Quarterly, Semi Annually, Annually |

|---|

Tools and Utilities That Simplify Tick-Data Backtesting in MT4

Popular data tools and tick simulators (Tickstory, Birt tools, etc.)

There are third-party tools that:

- Download and manage tick data.

- Create high-quality .fxt and .hst files.

- Integrate with MT4 to bypass some of its backtesting limitations.

When choosing a tool, consider:

- How easy it is to use.

- Whether it supports your broker’s MT4 build.

- Community feedback and documentation quality.

You can also explore official MetaQuotes resources and reputable trading communities for guidance and tutorials on specific utilities and workflows.

When to consider switching to MT5 or other platforms

MT4 is widely used, but:

- MT5 offers built-in tick data, multi-threaded testing, and more advanced tools.

- Other platforms support native tick-data backtesting and portfolio testing.

If you outgrow MT4’s limitations, migrating your EA logic to MT5 or another environment can be a smart long-term move.

Frequently Asked Questions About Tick-Data Backtesting in MT4

1. Do I really need tick data for every EA?

No. If your strategy:

- Enters and exits only on bar open.

- Uses wider stop losses and take profits.

- Trades on higher timeframes (H4, Daily).

Then high-quality bar data might be enough. Tick data is most critical for scalpers and systems sensitive to intra-bar moves.

2. Why does my modelling quality show only 90% instead of 99%?

The % shown in MT4 is based on how it reconstructs data internally. With good M1 data, 90% is normal. Some tools “force” 99% display when they know the backtest truly uses tick data. Focus more on data integrity and logical robustness than the displayed number alone.

3. Can I mix my broker’s data with external tick data?

You can, but it can cause mismatches. It’s better to:

- Use one consistent source for the tested period.

- Or carefully align time zones and symbol settings if you must mix.

4. How often should I update my tick data?

If you keep developing and retesting your EA, update regularly (weekly or monthly). This ensures you’re testing on the latest market conditions, including recent news events and volatility regimes.

5. Is optimization with tick data too slow?

It can be slow, especially on older hardware. To speed up:

- Use shorter date ranges for initial parameter sweeps.

- Narrow down promising ranges.

- Then run final, heavier tests on longer histories.

6. Can I use a VPS or separate machine just for backtesting?

Yes, that’s a good idea. A dedicated machine or VPS with a fast SSD and decent CPU lets you run large tick-data tests without slowing down your main trading setup.

Conclusion: Building Trustworthy MT4 EAs with Realistic Tick Backtests

Now you know how to backtest mt4 ea with tick data in a structured, professional way. By using a dedicated MT4 terminal, importing high-quality tick data, and carefully analyzing your backtest reports, you avoid the trap of “perfect” but unrealistic results. Instead, you get a clearer picture of how your EA might behave in real markets, including spread changes, news spikes, and random slippage.

Remember, a backtest is still only a model of reality. But when you combine robust tick-data testing, out-of-sample validation, and stress tests, you dramatically increase your chances of building an Expert Advisor you can trust with real capital.

Most Popular Forex EA

Onix Stratos XAUUSD EA: AI Smart Scalper for MT5

In stock

$0.00 $999.99Price range: $0.00 through $999.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $399.99Price range: $0.00 through $399.99

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

Zenith Matrix XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $899.99Price range: $0.00 through $899.99

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

In stock

$0.00 $797.99Price range: $0.00 through $797.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

In stock

Original price was: $109.99.$87.99Current price is: $87.99.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99

Gold Forex EA

Gold Forex EA