Kelly Criterion Formula in Trading: Risk Management Guide

The Kelly Criterion Formula in Trading is a powerful mathematical approach designed to help traders and investors maximize their long-term portfolio growth while minimizing risk. By carefully calculating the optimal size of each trade, the Kelly Criterion allows disciplined decision-making that balances reward and risk. Originally developed for gambling, this formula has found wide applications in the stock market, Forex, and cryptocurrency trading.

Introduction to the Kelly Criterion

Traders and investors often struggle with position sizing and risk management. Betting too little may lead to underperformance, while betting too much can quickly ruin a portfolio. This is where the Kelly Criterion comes in. Developed by John L. Kelly Jr. in 1956 at Bell Labs, it provides a systematic method for determining the ideal proportion of capital to risk on a trade or investment.

What is the Kelly Criterion?

The Kelly Criterion is a formula that calculates the optimal size of a bet based on the probability of winning and the ratio of potential profit to loss. It’s designed to maximize the geometric growth of your wealth over time.

History and Background

John L. Kelly Jr., a researcher at Bell Labs, originally designed the formula to improve data transmission efficiency. Soon after, it was applied to gambling and investing. The idea is simple: avoid over-betting while still capitalizing on a positive expected value.

The Kelly Criterion Formula Explained

The core Kelly formula is:f∗=bbp−q

Where:

- f* = fraction of capital to bet

- b = net odds received on the wager (profit per unit risked)

- p = probability of winning

- q = probability of losing (1 – p)

This formula helps traders determine the optimal allocation per trade to maximize growth and minimize risk of ruin.

Simplified Example for Traders

Imagine a trader has a strategy with:

- Probability of winning: 60% (p = 0.6)

- Potential profit per trade: 2:1 (b = 2)

- Probability of losing: 40% (q = 0.4)

Plugging into the Kelly formula:f∗=2(2×0.6)−0.4=21.2−0.4=0.4

This means the trader should risk 40% of their capital on this trade to maximize long-term growth.

Applying the Kelly Criterion in Trading

Using Kelly for Stock Trading

The Kelly formula is highly valuable in position sizing. Traders can calculate how much of their portfolio to risk on each stock based on historical win rates and expected returns. It helps avoid underexposure and reduces the chance of overleveraging.

Using Kelly in Forex and Crypto

For highly volatile markets like Forex and cryptocurrencies, the Kelly Criterion can guide leverage decisions and position sizing. Conservative traders often use fractional Kelly, betting only a portion of the recommended allocation to manage volatility.

Advantages of the Kelly Criterion in Trading

Optimizing Long-Term Growth

Kelly ensures that your capital grows at a geometric rate, compounding returns over multiple trades.

Reducing the Risk of Ruin

By calculating the optimal bet size, Kelly reduces the likelihood of bankruptcy, making it a powerful risk management tool.

Limitations and Risks of the Kelly Formula

Overestimation of Edge

Incorrect probability estimates can lead to overbetting, increasing losses.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99| Validity | Monthly, Quarterly, Semi Annually, Annually |

|---|

Adjusted or Fractional Kelly

Many traders use fractional Kelly (e.g., 50% Kelly) to reduce risk while still gaining growth advantages. This approach balances safety and profitability.

Practical Tips for Traders

Estimating Winning Probabilities

Traders should use historical data, backtesting, and statistical analysis to estimate the probability of success accurately.

Tools and Software for Kelly Calculations

Various platforms, including Excel, Python, and trading software, can automate Kelly calculations for daily trading.

Frequently Asked Questions (FAQs)

- Can the Kelly Criterion guarantee profits?

No, it only maximizes long-term growth based on probabilities; it doesn’t prevent losses. - What is fractional Kelly?

Fractional Kelly involves using a portion of the full Kelly bet to reduce volatility and risk. - Is Kelly suitable for beginners?

Yes, but accurate probability estimates are crucial. Beginners may start with fractional Kelly. - Can Kelly be used for Forex trading?

Absolutely. It helps in deciding position sizes and managing leverage in volatile markets. - Does Kelly work in cryptocurrency trading?

Yes, but due to high volatility, traders often use a conservative fractional Kelly approach. - How often should probabilities be updated?

Probabilities should be recalculated regularly based on market performance and historical data.

Conclusion

The Kelly Criterion Formula in Trading is a powerful tool for maximizing portfolio growth while controlling risk. By understanding the formula, applying it correctly, and considering fractional Kelly adjustments, traders can make disciplined, strategic decisions across various markets. Whether trading stocks, Forex, or crypto, integrating Kelly into your risk management strategy can significantly enhance long-term profitability.

Most Popular Forex EA

Onix Stratos XAUUSD EA: AI Smart Scalper for MT5

In stock

$0.00 $999.99Price range: $0.00 through $999.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $399.99Price range: $0.00 through $399.99

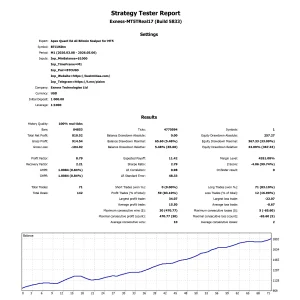

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

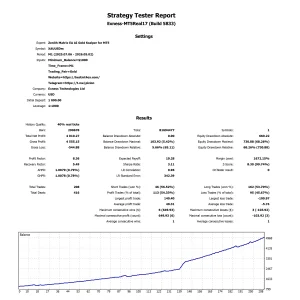

Zenith Matrix XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $899.99Price range: $0.00 through $899.99

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

In stock

$0.00 $797.99Price range: $0.00 through $797.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

In stock

Original price was: $109.99.$87.99Current price is: $87.99.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99

Gold Forex EA

Gold Forex EA