Kelly Criterion Position Sizing Explained

The Kelly Criterion is a mathematical formula used to determine the optimal size of a series of bets or investments, maximizing the growth of wealth over time while minimizing the risk of bankruptcy. Developed by John L. Kelly Jr. in 1956, it has since become an essential tool in gambling, investing, and trading.

The core idea behind the Kelly Criterion is to calculate the percentage of your capital to allocate to each investment or bet to optimize long-term growth, based on the potential odds or expected return. While it was originally applied to gambling, it has found widespread use in financial markets.

The Formula

The basic formula for the Kelly Criterion is:f∗=bbp−q

Where:

- f∗ is the fraction of the capital to bet or invest.

- b is the odds received on the bet (i.e., how much you will win relative to your stake).

- p is the probability of winning.

- q is the probability of losing (i.e., 1−p).

The formula gives the “optimal” bet size as a fraction of the current bankroll. The Kelly Criterion aims to find a balance between risking too much (which could lead to large drawdowns) and risking too little (which could limit potential returns).

Example: Applying the Kelly Criterion

Let’s break it down with an example. Suppose you’re an investor evaluating a stock trade.

- You believe there is a 60% chance (i.e., p=0.60) the stock will go up.

- If the stock does go up, you expect a 50% return on your investment (i.e., b=0.50).

- The probability of the stock going down is 40% (i.e., q=0.40).

Using the Kelly Criterion:f∗=0.500.50×0.60−0.40=0.500.30−0.40=−0.20

The result of −0.20 suggests that this is a losing proposition, meaning you should avoid making the trade.

Now let’s adjust the numbers:

- Let’s assume the probability of the stock going up is still 60%, but you expect a 100% return (i.e., b=1.00).

f∗=1.001.00×0.60−0.40=1.000.60−0.40=0.20

This result of 0.20 suggests you should allocate 20% of your capital to this particular stock trade to maximize long-term growth according to the Kelly Criterion.

Advantages of the Kelly Criterion

- Maximized Growth: The Kelly Criterion is designed to maximize the growth of capital over time by compounding returns optimally.

- Risk Management: It balances risk and reward, encouraging large enough bets to capture favorable opportunities, but not so large that a string of losses can wipe out your capital.

- Informed Decision-Making: It provides a rational framework based on probability and expected return, helping investors and traders make decisions with quantifiable data.

Limitations and Considerations

- Overestimating the Odds: The Kelly Criterion requires an accurate estimation of the probabilities and payoffs. If you misjudge the likelihood of success or potential returns, the bet size calculated might not reflect reality.

- Risk of Large Fluctuations: While the Kelly Criterion is optimal for long-term growth, it can lead to large fluctuations in the short term, especially in volatile markets. Many traders and investors prefer to use a “fractional Kelly,” betting a smaller portion of the optimal size to reduce volatility.

- Availability of Accurate Information: In real-world investing and trading, it’s often challenging to know the true probabilities and expected returns, which makes applying the formula perfectly difficult.

Fractional Kelly: A More Conservative Approach

To mitigate the risk of large drawdowns, many investors and traders use a fraction of the Kelly Criterion. For example, instead of betting the full f∗ derived from the formula, you might decide to only bet half of it (i.e., use 50% of the Kelly amount). This reduces the volatility of your portfolio and the risk of significant losses during a series of unfavorable outcomes.

A common variation is:ffractional=21×f∗

This strategy is widely used by professional traders to ensure steady, consistent growth without exposing themselves to large drawdowns.

Conclusion

The Kelly Criterion is a powerful tool for position sizing in both gambling and investing, providing a way to determine the optimal bet size or investment amount to maximize long-term growth. While it offers significant advantages in terms of maximizing returns and managing risk, it requires accurate assessments of probabilities and potential payoffs, which can be difficult in real-world conditions. For most investors and traders, a conservative approach using fractional Kelly can be an effective way to enjoy the benefits of the formula while minimizing the risks of volatility.

By incorporating the Kelly Criterion into your investment strategy, you can make more informed decisions, optimize the growth of your portfolio, and manage risk effectively.

Most Popular Forex EA

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

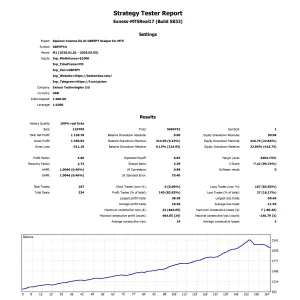

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

324 in stock

Original price was: $1,861.99.$187.99Current price is: $187.99.

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

47 in stock

$0.00 $797.99Price range: $0.00 through $797.99

Onix Stratos XAUUSD EA: AI Smart Scalper for MT5

In stock

$4.99 $999.99Price range: $4.99 through $999.99

Powerful Forex VPS for MT4 & MT5 – Best Price

182 in stock

$44.99 $359.99Price range: $44.99 through $359.99

Top 2000 Trading Tools for Forex Success (EA & Indicator)

In stock

Original price was: $99.99.$0.00Current price is: $0.00. Gold Forex EA

Gold Forex EA