11 Powerful Benefits of Walk Forward Optimization in Backtesting

Successful traders and algorithm developers know that a strategy is only as strong as its ability to survive real markets. That’s why walk forward optimization in backtesting has become a gold-standard method for validating trading systems. Instead of relying on a single static backtest, it uses repeated cycles of optimization and testing to create a more reliable, adaptive, and realistic measure of performance.

Markets change fast—trend periods, volatility regimes, crashes, and consolidations appear without warning. Walk forward optimization helps traders handle this uncertainty by testing how well a strategy adjusts across multiple market environments.

In this guide, we break down everything you need to know, from core concepts and step-by-step implementation to real examples and common mistakes to avoid.

Introduction to Walk Forward Optimization in Backtesting

Walk forward optimization in backtesting is a dynamic process used to validate a trading strategy by repeatedly optimizing it on one dataset and testing it on a different, unseen dataset. This method helps traders judge whether a strategy can hold up under varying market conditions rather than just a fixed period.

Why Traditional Backtesting Falls Short

Traditional backtesting often produces impressive results—until the strategy goes live. That’s because static backtests suffer from:

- Curve fitting

- Look-ahead bias

- Unrealistic assumptions

- Over-optimized parameters

- Lack of adaptation to market regime shifts

These weaknesses cause strategies to break when markets behave differently than the test period.

How Walk Forward Analysis Solves These Challenges

Walk forward optimization addresses these issues by:

- Using multiple cycles of testing

- Separating training and testing periods

- Ensuring models adapt to new conditions

- Reducing reliance on historical quirks

This leads to a more trustworthy performance record.

Understanding the Core Concept of Walk Forward Optimization

At its heart, walk forward optimization is simple:

Optimize on past data → Test on unseen data → Move forward → Repeat

This generates a sequence of out-of-sample results that better mimic real trading.

In-Sample vs Out-of-Sample Data

| Term | Meaning |

|---|---|

| In-Sample (IS) | Data used for optimization or training |

| Out-of-Sample (OOS) | Data used for performance validation |

A proper walk forward test uses many of these IS/OOS cycles.

Avoiding Look-Ahead Bias & Overfitting

Walk forward testing blocks future data from influencing optimization. This ensures:

- No cheating in the model

- Less curve fitting

- More robust strategies

Step-by-Step Process of Walk Forward Optimization in Backtesting

Let’s break down the full workflow.

Step 1 – Select a Trading Strategy

This can be:

- A moving average crossover

- A breakout system

- A machine learning model

- A mean reversion algorithm

The method works for both simple and complex strategies.

Step 2 – Define Optimization Parameters

These may include:

- Indicator lookback periods

- Stop-loss and take-profit levels

- Entry/exit triggers

- Position sizing rules

Choose only essential parameters—too many cause overfitting.

Step 3 – Conduct In-Sample Optimization

The model is trained on a historical window such as:

- 1 year

- 18 months

- 3 years

The goal: find the best-performing parameters.

Step 4 – Perform Out-of-Sample Testing

Next, apply the optimized parameters to a new dataset that was not used during optimization. This shows how the strategy might perform in the future.

Step 5 – Roll Forward and Repeat

Shift both windows forward and repeat the process. Eventually, you get a fully stitched-together out-of-sample performance record representing many market conditions.

Types of Walk Forward Optimization Approaches

Anchored Walk Forward Optimization

Starts at a fixed point and expands IS data forward while OOS remains fixed.

Rolling Window Walk Forward Optimization

Both IS and OOS periods shift forward by the same window length.

Expanding Window Optimization

IS window grows while OOS length stays constant.

Advantages of Using Walk Forward Optimization in Backtesting

Reduces Overfitting and Curve Fitting

Walk forward methods limit the impact of noisy historical data.

Improves Real-World Reliability

Because each OOS segment simulates live conditions.

Enhances Adaptability to Market Conditions

New parameter sets are continually updated to reflect market changes.

Common Mistakes to Avoid

Using Too Many Parameters

This leads to curve fitting and poor future performance.

Insufficient Out-of-Sample Data

OOS windows should be long enough to capture realistic volatility.

Ignoring Transaction Costs

Commissions, spreads, and slippage must be included.

Tools and Platforms That Support Walk Forward Optimization

Some popular platforms include:

- MetaTrader 5

- AmiBroker

- TradeStation

- QuantConnect

- Python libraries (Backtrader, Zipline)

For more details, you may explore:

🔗 https://www.investopedia.com (reputable financial education source)

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99| Validity | Monthly, Quarterly, Semi Annually, Annually |

|---|

Real Example: Applying Walk Forward Optimization in Backtesting

Imagine optimizing a breakout strategy:

- IS window: 2 years

- OOS window: 3 months

- Parameters: breakout length 20–100, stop-loss 1–5%

Run repeated cycles, evaluate OOS performance, and adjust accordingly.

This yields a stable performance curve across multiple market regimes.

Frequently Asked Questions

1. What is walk forward optimization in backtesting?

It’s a process that repeatedly optimizes and tests a strategy on separate data windows to reduce overfitting and improve robustness.

2. Why is walk forward better than a single backtest?

Because it simulates real-time strategy updates and avoids relying on a single historical period.

3. How long should in-sample and out-of-sample windows be?

Typical setups use 1–3 years IS and 1–6 months OOS, but it depends on the strategy.

4. Does walk forward optimization guarantee profits?

No method can guarantee profits, but it substantially increases the reliability of backtests.

5. Can machine learning models use walk forward analysis?

Yes—ML models benefit greatly because they require strict separation between training and validation data.

6. Does walk forward testing work for crypto and forex?

Yes, it works across all asset classes including stocks, futures, forex, and crypto.

Conclusion

Walk forward optimization in backtesting is one of the most powerful ways to validate a trading strategy in an ever-changing market. By continually updating parameters, separating training from testing data, and simulating live conditions, traders gain a clearer picture of how a strategy performs under real pressure.

Whether you’re a systematic trader, quant developer, or algorithmic researcher, walk forward testing is an essential tool for building robust and reliable strategies.

Most Popular Forex EA

Onix Stratos XAUUSD EA: AI Smart Scalper for MT5

In stock

$0.00 $999.99Price range: $0.00 through $999.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $399.99Price range: $0.00 through $399.99

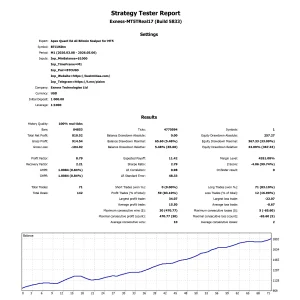

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

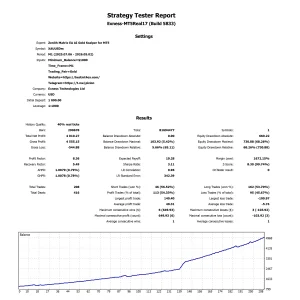

Zenith Matrix XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $899.99Price range: $0.00 through $899.99

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

In stock

$0.00 $797.99Price range: $0.00 through $797.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

In stock

Original price was: $109.99.$87.99Current price is: $87.99.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99

Gold Forex EA

Gold Forex EA