7 Powerful Ways monte carlo simulation for strategy testing Can Dramatically Improve Your Decisions

H1: Understanding monte carlo simulation for strategy testing in Simple Terms

In real life, almost every strategy faces uncertainty. Markets move in surprising ways, customers change their minds, projects hit delays, and costs sometimes explode out of nowhere. Instead of asking, “What will happen?” a better question is, “What could happen, and how often?”

That’s where monte carlo simulation for strategy testing comes in. It’s a way of using random numbers and probability to test how a strategy might perform under thousands of different possible futures. Rather than getting just one answer, you get a whole range of outcomes – from great to terrible – and see how likely each one is.

This approach helps you move away from guesswork and “single-scenario thinking” and move toward decisions grounded in risk awareness, probabilities, and data.

H2: What Is Monte Carlo Simulation? A Clear Overview

At its core, a Monte Carlo simulation is a method that uses repeated random sampling to estimate the outcomes of uncertain processes. You build a model that describes how your system behaves – a trading strategy, an investment portfolio, a product launch, or a large project. Then you let the computer feed in random draws for the uncertain parts and run the model again and again, sometimes thousands or millions of times.

Each run of the model is one possible future. When you look at many runs together, you get a probability-based view of the future rather than a single forecast. This is incredibly useful for strategy testing because strategies don’t fail only in “average” conditions. They usually break in rare, stressful, or unlikely scenarios.

H3: The Core Idea: Randomness, Risk, and Repeated Trials

Monte Carlo simulation leans on three simple ideas:

- Randomness: Many variables you care about can’t be predicted exactly – prices, demand, delays, interest rates, or volatility.

- Risk: Because outcomes are uncertain, you face downside risk (losses, delays, cost overruns) and upside potential (profits, early deliveries, big wins).

- Repeated trials: By simulating thousands of random paths, you can estimate how often each level of profit, loss, or performance might occur.

When combined, these moves you away from “one forecast” and toward a probability map of outcomes.

H3: Key Concepts: Scenarios, Distributions, and Outcomes

A Monte Carlo simulation uses:

- Scenarios – Each run is one scenario, one possible path the world might take.

- Probability distributions – Instead of fixed values, you assign variables a distribution (for example, demand could be normally distributed, or returns might follow a fat-tailed distribution).

- Outcome metrics – You track what you care about: total profit, maximum drawdown, project completion date, customer churn, or portfolio value.

After many runs, you can see, for example, “There’s a 90% chance that the project finishes before this date,” or “There’s a 5% chance of losing more than this amount.”

H2: Why Use Monte Carlo for Strategy Testing Instead of Simple Backtesting?

Most people start with backtesting or basic scenario analysis. They look at how a trading strategy, portfolio, or business plan would have done in the past or under one or two scenarios. This is helpful but often incomplete.

H3: Limits of Historical Backtests and Static Scenarios

Backtests and simple scenarios have several weaknesses:

- They rely on past data, which might not reflect future conditions.

- They often use single paths – one set of prices, one set of customer numbers, one timeline.

- They ignore uncertainty in assumptions (for example, costs “assumed” to be fixed).

- They rarely show how bad things can get when rare events occur.

This can give a false sense of security: the strategy looks safe under neat, tidy assumptions, but collapses under more extreme, but still realistic, conditions.

H3: How Simulations Reveal Hidden Risks and Tail Events

Monte Carlo simulations allow you to:

- Explore a wide range of futures, including rare and extreme ones.

- See distributions of results, not just averages.

- Measure tail risks, such as “What’s the 1% worst-case outcome?”

This helps you spot strategies that look good on the surface but are fragile underneath.

H2: Building Blocks of a Monte Carlo Simulation Model

H3: Defining Inputs: Variables, Ranges, and Probability Distributions

Every simulation starts with your model inputs:

- Identify key uncertain variables (e.g., daily return, customer demand, project delay).

- Define a range and shape for each variable.

- Choose a probability distribution (e.g., normal, lognormal, triangular, uniform).

In practice, you might estimate these from historical data, expert judgment, or industry benchmarks.

H3: Running Thousands of Trials for One Strategy

Once inputs are defined:

- Generate random values for each uncertain variable.

- Run your model to calculate the result for that trial.

- Repeat thousands of times.

The result is a large set of simulated outcomes showing what could happen if you followed the same strategy in many different futures.

H3: Summarizing Results: Averages, Percentiles, and Worst-Case Paths

From these outcomes you can calculate:

- Average result – a central tendency (e.g., mean profit).

- Percentiles – for example, the 5th percentile profit (a “bad case”) and 95th percentile profit (a “great case”).

- Risk metrics – maximum drawdown, risk of ruin, chance of hitting a target, etc.

This lets you talk in probabilities, not guesses.

H2: Using monte carlo simulation for strategy testing in Trading and Investing

In trading and investing, uncertainty is everywhere. Prices move, volatility changes, correlations shift. Strategy testing with simulations helps you see how robust your ideas are.

H3: Position Sizing, Drawdowns, and Risk of Ruin

You can simulate:

- Sequences of wins and losses.

- Different bet sizes or position sizing rules.

- Account equity over time.

From this, you estimate:

- Probability of drawdowns of a certain size.

- Risk of ruin – the chance of losing most or all of your capital.

- Sustainable position sizes that keep risk under control.

H3: Testing Portfolio Strategies Under Market Stress

You can model:

- Shocks to returns (crashes or spikes).

- Changes in correlations during crises.

- Different rebalancing rules.

This helps you answer questions like, “How would this portfolio behave if we saw a crash similar to past events, but combined with higher interest rates?”

H3: Evaluating Algorithmic Trading Rules and Parameters

For algo strategies, you might:

- Randomize order of trades to see sequencing risk.

- Vary volatility, spread, and slippage.

- Test slightly different parameter sets to see sensitivity.

This helps you avoid overconfidence in a single, finely-tuned backtest.

H2: Monte Carlo in Business Strategy and Project Planning

Simulation isn’t just for finance. It’s equally powerful in business and operations.

H3: Scenario Planning for Revenue and Costs

You can model:

- Sales volumes with uncertainty.

- Price changes.

- Variable and fixed costs.

This lets you estimate the distribution of profit instead of one single projected number.

H3: Project Timelines, Budgets, and Resource Risks

For projects, you can:

- Assign best, most likely, and worst-case durations to tasks.

- Simulate how these combine in complex project plans.

- Estimate the probability of finishing before a deadline or staying inside budget.

Project managers often use this to set more realistic contingency buffers.

H3: Capital Allocation and Strategic Decisions

Executives can simulate:

- Returns on different strategic options.

- Risk of cash shortfalls under different investment plans.

- Impact of downside scenarios on long-term goals.

This supports better capital allocation and more resilient strategies.

H2: Step-by-Step: How to Set Up Your First Monte Carlo Strategy Test

H3: Step 1: Define the Objective and Time Horizon

Clarify:

- What decision you’re testing (e.g., “Should we deploy this trading strategy?”).

- What metric matters (profit, drawdown, completion time, etc.).

- Over what period you’re evaluating the strategy.

H3: Step 2: Identify Key Uncertain Variables

List variables that can move unpredictably, such as:

- Market returns.

- Customer demand.

- Lead times and delays.

- Cost inflation.

Leave out minor details at first; focus on what really drives results.

H3: Step 3: Choose Suitable Distributions for Each Variable

For each variable:

- Decide its range.

- Pick a distribution based on data or expert input.

- Check that assumptions make sense in the real world.

H3: Step 4: Run the Simulation and Store Results

Use software or a spreadsheet to:

- Generate random values.

- Run the model automatically many times.

- Save key outputs from each run.

H3: Step 5: Analyze the Distribution of Outcomes

Look at:

- Histograms of results.

- Percentiles (for example, 10th, 50th, 90th).

- Worst-case and best-case runs.

Ask: “Is this strategy acceptable under the kinds of risks we see here?”

H2: Interpreting Simulation Results Without Getting Overwhelmed

H3: Reading Histograms, Confidence Intervals, and Percentiles

A histogram shows how often different ranges of outcomes appear. Clusters show what’s likely; long tails can signal rare but extreme events. Confidence intervals help you say things like, “We’re 95% confident the result lies between X and Y under these assumptions.”

H3: How to Translate Results into Practical Decisions

Use the results to:

- Adjust strategy rules (smaller positions, tighter limits).

- Add buffers (extra capital, time, or inventory).

- Choose between options (pick strategies with acceptable risk-return profiles).

The goal isn’t to predict the future perfectly, but to avoid being surprised by risks you could have seen.

H2: Common Mistakes When Using Monte Carlo in Strategy Testing

H3: Using Unrealistic Assumptions and Distributions

If your assumptions are wrong, your simulation will be misleading. Avoid:

- Overly narrow ranges.

- “Nice, neat” distributions that ignore fat tails.

- Assumptions that contradict real-world data.

H3: Ignoring Correlations Between Variables

Many variables move together. For example:

- Markets may fall together in crises.

- Costs may rise when demand spikes.

If you ignore correlations, you might underestimate risk.

H3: Overfitting and False Sense of Certainty

Don’t tweak the model endlessly to get “nice” results. Simulations are tools for exploring uncertainty, not for painting a perfect picture. Always remember: the model is only an approximation.

H2: Simple Tools and Software Options to Run Monte Carlo Simulations

H3: Spreadsheets (Excel, Google Sheets, LibreOffice)

Spreadsheets can:

- Use built-in random number functions.

- Implement simple models quickly.

- Plot histograms and charts.

They’re a good starting point for small problems.

H3: Specialized Risk and Simulation Software

Dedicated tools offer:

- Easy setup for complex models.

- Built-in distributions and risk metrics.

- Better visualization and reporting.

Many project managers and financial analysts use such tools daily.

H3: Programming Languages and Libraries (Python, R, etc.)

For complex or large-scale problems, coding is powerful. Python, for example, has strong libraries for statistics, data handling, and visualization. You can automate big simulations and apply more advanced techniques. A good starting point for general learning is the material at the free courses hosted by reputable universities and platforms, which you can find via sites like the ones linked from Khan Academy’s statistics and probability section.

H2: Case Study: Testing a Simple Trading Strategy with Monte Carlo

H3: Defining the Strategy and Risk Parameters

Imagine a simple strategy:

- It wins 55% of the time.

- Average win is slightly larger than average loss.

- You risk 1% of your account per trade.

You want to know: “What’s the chance this strategy blows up my account or suffers a painful drawdown?”

H3: Simulating Trade Sequences and Equity Curves

You can:

- Simulate thousands of trade sequences (e.g., 500 trades per run).

- Randomly assign wins and losses based on the win rate.

- Track account balance over each simulated sequence.

Over many runs, you see many possible equity curves, not just one.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99| Validity | Monthly, Quarterly, Semi Annually, Annually |

|---|

H3: Reading the Results and Adjusting the Rules

From the simulation, you might discover:

- Some paths grow smoothly.

- Some paths struggle but recover.

- A small percentage of paths suffer large drawdowns.

If the worst cases are too painful, you might:

- Cut position size to 0.5% per trade.

- Add a rule to pause trading after a certain drawdown.

- Reconsider stop levels or profit targets.

This kind of analysis makes your risk choices conscious and deliberate.

H2: When You Should NOT Rely Only on Monte Carlo Simulations

H3: Structural Breaks, Black Swans, and Model Blind Spots

No model can capture every surprise. Structural changes – like new technologies, regulations, or wars – can make past-based assumptions unreliable. Black swan events, by definition, sit outside common expectations.

Simulations can’t fully protect you from unknown unknowns, so humility is essential.

H3: The Need for Judgment, Experience, and Qualitative Insight

Good decision-making blends:

- Quantitative analysis (like Monte Carlo).

- Qualitative understanding (industry knowledge, common sense).

- Ethical and strategic thinking.

Models support human judgment; they don’t replace it.

H2: Best Practices to Make Your Strategy Testing More Reliable

H3: Stress Testing, Sensitivity Analysis, and Scenario Design

Combine Monte Carlo with:

- Stress tests – push variables to extremes.

- Sensitivity analysis – see which inputs matter most.

- Hand-built scenarios – explore specific “what if” stories.

This helps you understand both everyday risk and extraordinary situations.

H3: Combining Backtesting, Monte Carlo, and Expert Review

A robust process will:

- Backtest your strategy to see how it behaved historically.

- Use monte carlo simulation for strategy testing to explore many possible futures.

- Involve experts who can question assumptions and suggest realistic scenarios.

Together, these steps can make your strategy much more resilient.

H2: FAQs About Monte Carlo Simulation in Strategy Testing

Q1. Is Monte Carlo simulation only for finance and trading?

No. It’s widely used in engineering, project management, energy, manufacturing, research, and more. Any field with uncertainty can benefit.

Q2. How many simulation runs do I need?

There’s no magic number, but thousands of runs are common. More runs give smoother and more stable estimates, but also require more computing power.

Q3. Do I need advanced math to use Monte Carlo?

You need a basic understanding of probability and distributions, but not advanced calculus. Many tools hide the complex math behind a user-friendly interface.

Q4. Can Monte Carlo tell me exactly what will happen?

No. It doesn’t predict the future. It estimates possible futures and their probabilities based on your assumptions. It’s a tool for understanding risk, not fortune-telling.

Q5. How do I know my simulation is realistic?

Check your assumptions against real data, talk to domain experts, and see if the simulated results resemble known historical patterns. If they don’t, revisit your input distributions and model logic.

Q6. Is a strategy safe if Monte Carlo shows low risk?

Not automatically. Low risk in the model assumes your inputs and structure are correct. Always allow for model error, unexpected events, and human mistakes when deciding how much to risk.

H2: Conclusion: Turning Uncertainty Into Informed Strategy Choices

Uncertainty can feel scary, but it doesn’t have to be paralyzing. With tools like monte carlo simulation for strategy testing, you can explore a wide range of futures, understand your risks, and choose strategies that fit your goals and risk tolerance.

Most Popular Forex EA

Onix Stratos XAUUSD EA: AI Smart Scalper for MT5

In stock

$0.00 $999.99Price range: $0.00 through $999.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $399.99Price range: $0.00 through $399.99

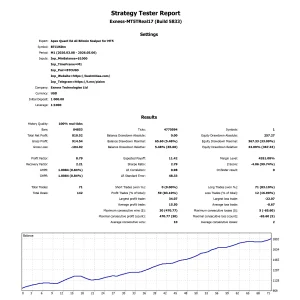

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

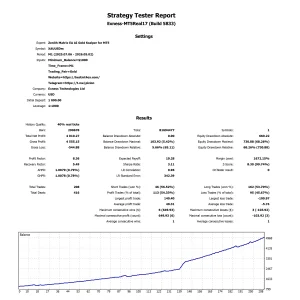

Zenith Matrix XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $899.99Price range: $0.00 through $899.99

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

In stock

$0.00 $797.99Price range: $0.00 through $797.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

In stock

Original price was: $109.99.$87.99Current price is: $87.99.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99

Gold Forex EA

Gold Forex EA