9 Powerful Ways to Master How to Calculate Sharpe Ratio for Forex EAs (Guaranteed Performance Boost)

How to Calculate Sharpe Ratio for Forex EAs: 9 Powerful Steps for Better Trading Performance

Introduction to how to calculate sharpe ratio for forex eas

If you want to truly understand whether a Forex Expert Advisor (EA) is performing well, you need more than a simple profit figure. You need a metric that shows how much risk your EA takes to earn its profits. That’s where knowing how to calculate sharpe ratio for forex eas becomes incredibly valuable. This ratio gives traders a clearer picture of efficiency, stability, and long-term viability.

By mastering this calculation, you can compare EAs, optimize strategies, and filter out systems that look good on paper but fail when risk is considered.

What Is the Sharpe Ratio? A Simple Explanation

The Sharpe Ratio measures how much excess return a trading strategy earns for each unit of risk it takes. It helps determine whether an EA’s high returns are due to skill or simply luck and volatility.

Why the Sharpe Ratio Matters for Forex Traders

- It reveals if an EA is stable or unpredictable.

- It helps compare two EAs—even when their returns differ.

- It allows traders to spot hidden risks in overly aggressive systems.

The Connection Between Profitability and Risk

Many EAs appear highly profitable because they use risky tactics like martingale or grid systems. The Sharpe Ratio exposes when returns come with dangerous volatility.

Understanding Forex Expert Advisors (EAs) and Their Risk Profiles

Forex EAs automate trading by executing rules and algorithms in the market. Each EA carries a unique pattern of risk.

How EAs Generate Trading Signals

- Trend-following logic

- Mean-reversion systems

- Breakout strategies

- News-based algorithms

Why Performance Metrics Are Essential

Strong backtests don’t guarantee future success. The Sharpe Ratio reveals an EA’s resilience during market stress—something profit alone cannot show.

Components Needed to Calculate the Sharpe Ratio

Before you calculate the ratio, you must gather the right numbers.

Determining Expected Returns for Forex EAs

Use daily, weekly, or monthly returns. Weekly or monthly returns give a cleaner view for long-term EA evaluation.

Measuring Return Volatility (Standard Deviation)

Standard deviation shows how “bumpy” or variable your EA’s returns are over time.

Choosing an Appropriate Risk-Free Rate

Many traders use:

- U.S. Treasury yields

- 0% (common for simplicity in FX backtests)

Step-by-Step Guide: How to Calculate the Sharpe Ratio for Forex EAs

Let’s break down the calculation so even beginners can follow it confidently.

Step 1: Collect EA Performance Data

Gather periodic returns—daily or weekly percentage gains or losses.

Step 2: Compute Average Returns

Average Return = (Sum of returns ÷ Number of periods)

Step 3: Calculate Standard Deviation of Returns

This measures how much your returns vary.

Step 4: Apply the Sharpe Ratio Formula

Sharpe Ratio=Standard DeviationAverage Return−Risk Free Rate

Practical Example Calculation

Assume:

- Average weekly return = 2%

- Standard deviation = 1%

- Risk-free rate = 0%

Sharpe=0.010.02−0=2.0

A Sharpe Ratio of 2.0 is considered excellent for Forex EAs.

What Is a Good Sharpe Ratio for Forex EAs?

Industry Benchmarks

| Sharpe Ratio | Meaning |

|---|---|

| < 0 | Losing strategy |

| 0–0.99 | Weak performance |

| 1–1.99 | Acceptable; moderate risk |

| 2–2.99 | Strong performance |

| 3+ | Outstanding and rare |

How Market Conditions Affect the Ratio

High volatility environments naturally lower the Sharpe Ratio due to inconsistent returns.

Common Mistakes When Calculating the Sharpe Ratio

Ignoring Compounding Effects

Daily data might exaggerate volatility; weekly or monthly data can provide smoother accuracy.

Using Unrealistic Risk-Free Rates

Avoid outdated rates—use current yield benchmarks.

Misinterpreting Negative Sharpe Ratios

Negative values indicate you’re losing money with more risk than reward.

Advanced Alternatives to the Sharpe Ratio

Sortino Ratio

Focuses only on downside volatility.

Calmar Ratio

Uses maximum drawdown instead of standard deviation.

Omega Ratio

Measures probability of returns above a chosen threshold.

How to Improve the Sharpe Ratio of Your Forex EAs

Reducing Drawdowns

Lower risk settings boost stability.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99| Validity | Monthly, Quarterly, Semi Annually, Annually |

|---|

Optimizing Entry and Exit Logic

Cleaner signals reduce noise and volatility.

Using Position Sizing Strategies

Techniques like fractional sizing balance risk and reward.

FAQs About how to calculate sharpe ratio for forex eas

1. Do I need special software to calculate the Sharpe Ratio?

No. Excel, Google Sheets, and MT4/MT5 reports provide enough data.

2. Should I use daily or weekly returns?

Weekly gives smoother results and is preferred for EA evaluation.

3. What if my Sharpe Ratio is negative?

It means your strategy is underperforming while taking risk—usually a sign to stop trading.

4. Can two EAs have the same Sharpe Ratio?

Yes, but one may have higher profit with higher risk. Always check drawdowns too.

5. Is a high Sharpe Ratio always good?

If it’s unnaturally high, the EA may be curve-fit or using martingale tactics.

6. Why is the risk-free rate often set to zero in Forex?

Forex carries minimal interest rate comparison value, so traders simplify with 0%.

Conclusion

Learning how to calculate sharpe ratio for forex eas gives traders a powerful advantage. You can easily compare EAs, uncover hidden risks, and choose systems that deliver stable, reliable returns—not just flashy profits. The Sharpe Ratio remains one of the best tools for identifying truly robust and sustainable automated trading strategies.

Most Popular Forex EA

Onix Stratos XAUUSD EA: AI Smart Scalper for MT5

In stock

$0.00 $999.99Price range: $0.00 through $999.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $399.99Price range: $0.00 through $399.99

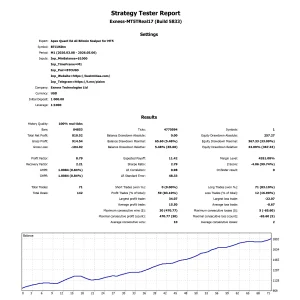

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

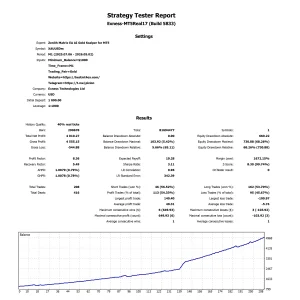

Zenith Matrix XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $899.99Price range: $0.00 through $899.99

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

In stock

$0.00 $797.99Price range: $0.00 through $797.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

In stock

Original price was: $109.99.$87.99Current price is: $87.99.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99

Gold Forex EA

Gold Forex EA