monte carlo simulations for mt4 robots: Complete Beginner-to-Pro Guide

If you use expert advisors on MetaTrader 4, you already know how exciting automated trading can be. You press “Start,” your MT4 robot takes trades for you, and the backtest equity curve looks amazing.

But here’s the big problem: real markets are messy, random, and often brutal. A strategy that looks perfect in a straight-line backtest can fall apart once it meets live spreads, slippage, and changing volatility. That’s where monte carlo simulations for mt4 robots come in.

Monte Carlo methods help you stress test your strategies against thousands of “what if” scenarios. Instead of relying on one perfect backtest, you see a range of possible futures. This gives you something every trader craves: realistic expectations and stronger confidence.

Understanding the Basics: What Are Monte Carlo Simulations?

Randomness, Probability, and Trading Systems

A Monte Carlo simulation is a way to model uncertainty using random sampling.

In trading terms, you take the trade results from your backtest and then:

- Randomly shuffle them

- Randomly change some outcomes

- Randomly adjust things like spread or slippage

You repeat this many times (hundreds or thousands of runs) to see how the equity curve might look under different conditions.

Instead of one single equity curve, you get a cloud of possible equity curves. From this cloud, you can estimate:

- How often you might hit a certain drawdown

- How likely it is to reach a target profit

- How sensitive your system is to small changes in the market

This turns your EA from a “backtest fantasy” into a statistically tested trading system.

Why Historical Backtests Alone Can Mislead You

Historical backtests are useful, but they have traps:

- The trade order is fixed and often “too perfect”

- Market conditions in that period may never repeat

- You might unconsciously tune your robot to that exact dataset

So a smooth equity curve might just mean your robot is curve-fitted to one special stretch of history. Monte Carlo shakes that curve to see what happens when the market doesn’t cooperate in the same neat way.

How MT4 Robots (Expert Advisors) Really Work Behind the Scenes

Trade Logic, Inputs, and Parameters

MT4 robots (expert advisors) are programs written in MQL4. They:

- Read price data (ticks, bars)

- Apply your rules (indicators, price action, time filters)

- Open, manage, and close trades automatically

You can configure parameters such as:

- Lot size or risk per trade

- Indicator periods (e.g., MA 50, MA 200)

- Time filters (London session only, etc.)

These parameters are often optimized using backtests. But over-optimization is where many traders get in trouble.

The Role of Historical Data in EA Testing

In MT4, you typically:

- Load historical price data

- Run a backtest in Strategy Tester

- Adjust settings to improve results

The issue: this process can lock your robot into the past. Monte Carlo breaks this lock by asking, “What if the past had been slightly different?” If small changes destroy performance, your EA may not be ready for live trading.

For official details about how MT4 and Strategy Tester work, you can check the MetaQuotes documentation.

Why monte carlo simulations for mt4 robots Matter So Much

Finding the “True” Risk of Your Strategy

When you run Monte Carlo tests, you’re not just chasing big profits. You’re trying to see:

- What’s my realistic maximum drawdown?

- How often could that drawdown occur?

- Is my system robust, or did I just get lucky in one backtest?

This kind of analysis helps you size your positions and choose safe risk levels. It’s much easier to keep calm during a losing streak when you know, “The Monte Carlo tests already showed this could happen.”

Overfitting, Curve-Fitting, and Hidden Weaknesses

Overfitting happens when an EA is tuned to the exact highs and lows of historical data. It looks amazing on paper but fails in live markets.

Monte Carlo helps expose overfitted systems because:

- Randomizing trade order may create new worst-case drawdowns

- Small changes in inputs might destroy profitability

- Slippage or spread changes may turn profits into losses

If your EA collapses under these tests, it’s a sign you need to simplify or redesign it.

Core Types of Monte Carlo Tests You Can Run on MT4 EAs

Randomizing Trade Order

This is one of the simplest and most powerful tests. You:

- Keep the same list of trade results (profit or loss per trade)

- Randomly shuffle the order many times

This shows you how bad the worst losing streaks could get if unlucky trades happen back to back. It’s critical for understanding your psychological and account risk.

Randomizing Trade Outcomes and Slippage

You can also:

- Slightly reduce some winning trades

- Slightly increase some losing trades

- Add random slippage or commissions

This simulates imperfect execution and more realistic trading conditions. If your EA only makes money when every entry and exit is perfect, Monte Carlo will reveal that.

Parameter and Spread Randomization

Some tools let you:

- Randomly vary indicator periods or thresholds

- Randomly change spread values during tests

This shows how sensitive your system is to small parameter changes and changing market costs. A robust EA should still survive, or at least remain profitable, under reasonable random variations.

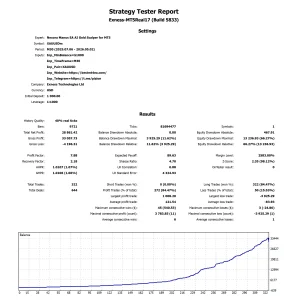

Step-by-Step: Running Monte Carlo Tests on Your MT4 Robot

Step 1: Prepare a High-Quality Backtest

Before any Monte Carlo simulation, you need a solid backtest:

- Use high-quality historical data

- Aim for 99% modeling quality if possible

- Cover multiple years and different market conditions

Make sure you include realistic:

- Spread

- Commission (if any)

- Slippage (if your broker tends to slip orders)

Step 2: Export Trade History for Simulation

Most workflows involve exporting the trade list:

- From MT4 Strategy Tester report

- Or from your account history if you use live data

You’ll usually export to CSV or HTML, then import this file into a Monte Carlo tool.

Step 3: Choose a Monte Carlo Tool or Plugin

There are several ways to run monte carlo simulations for mt4 robots:

- Standalone desktop tools that import your trade list

- Dedicated strategy testing platforms with built-in Monte Carlo

- MT4 scripts or external analyzers that focus on EA robustness

When choosing a tool, look for:

- Ability to randomize trade order, size, outcomes

- Graphs of drawdown distribution and equity clouds

- Multiple simulation runs (500+ is a good starting point)

Step 4: Configure the Simulation Scenarios

In your Monte Carlo tool, you might set:

- Number of simulations (e.g., 1,000 runs)

- Type of randomness (shuffle only, shuffle + outcome distortion, etc.)

- Level of variation (e.g., ±10% random change to each trade)

Start with conservative changes. Then gradually increase the “stress level” to see at which point your EA breaks.

Step 5: Interpret Key Outputs and Metrics

After running the simulations, focus on:

- Worst-case and median maximum drawdown

- Probability of the account reaching a given drawdown

- Distribution of final profits after X trades

- Range of equity curves

You’re not looking for perfection. You’re looking for consistency and survivability under stress.

Key Metrics to Watch During Monte Carlo Analysis

Maximum Drawdown and Drawdown Distribution

Maximum drawdown is the largest percentage drop from a peak to a trough in your equity. In Monte Carlo, you’ll see a range:

- Some runs may show small drawdowns

- Others may show much larger “bad luck” drawdowns

If many runs show extreme drawdowns (e.g., 60–70%), your risk settings are likely too aggressive.

Equity Curve Stability and Recovery Factor

Watch for:

- How smooth or choppy the equity curves are

- How quickly the system recovers from drawdowns

Recovery factor is the ratio of total net profit to maximum drawdown. Higher is better. A robust EA should keep a decent recovery factor in most Monte Carlo runs, not just in the original backtest.

Win Rate, Profit Factor, and Expectancy Ranges

Monte Carlo can show you ranges for:

- Win rate (e.g., 45–55%)

- Profit factor (e.g., 1.2–1.5)

- Expectancy per trade

These ranges help you set realistic expectations. If your backtest shows a win rate of 60%, but Monte Carlo suggests that 50% is more likely, you’ll be mentally prepared when live trading matches the lower number.

Practical Examples: Interpreting Different Monte Carlo Outcomes

A Stable, Robust EA – What It Looks Like in Monte Carlo

A strong system will typically show:

- Most equity curves sloping upward over time

- Drawdowns that stay within a manageable band

- Profit factor staying above 1.1 or 1.2 in many runs

The worst cases might still be uncomfortable, but they’re not catastrophic. This is the kind of EA you can trade with confidence, especially if you use conservative position sizing.

A Fragile, Overfitted EA – Warning Signs in the Results

A weak or overfitted EA often shows:

- Many simulations ending in flat or negative equity

- Massive spikes in maximum drawdown in some runs

- Profit factor dropping below 1 in a lot of simulations

If Monte Carlo keeps showing disaster scenarios, no matter how you tweak parameters, it’s usually better to rebuild the system than to force it live.

Best Practices for Using monte carlo simulations for mt4 robots in Live Trading

Position Sizing and Risk per Trade

Use Monte Carlo results to adjust:

- Risk per trade (for example, 0.5–1% instead of 3–5%)

- Maximum allowed exposure across pairs or strategies

If simulations show that a 2% risk per trade leads to huge drawdowns in bad luck scenarios, lower your risk so the “worst-case” is something you can survive.

Setting Realistic Profit and Drawdown Expectations

Monte Carlo can answer:

- “What kind of monthly returns are realistic?”

- “What’s a normal drawdown vs. a danger-level drawdown?”

This keeps your expectations grounded. When you know a 20% drawdown is possible and still statistically normal, you won’t panic and abandon a good system too early.

When to Turn Off or Adjust a Robot

If live performance moves far outside the Monte Carlo range (for example, much deeper drawdowns or constant losses), it may be a sign that:

- Market conditions changed dramatically

- The edge is gone

- Execution quality is much worse than expected

You can then pause, reduce risk, or re-evaluate the strategy.

Common Mistakes Traders Make With Monte Carlo and MT4 Robots

Running Too Few Simulations

If you only run 20 or 30 simulations, the range of results may still be misleading. Aim for:

- At least 500 runs, preferably 1,000+

More runs give you a better picture of the true risk distribution.

Ignoring Execution Costs and Slippage

If your Monte Carlo tests are based on a backtest that ignores:

- Realistic spread

- Commission

- Slippage

Then the results will be overly optimistic. Always start with realistic assumptions in your original backtest.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99| Validity | Monthly, Quarterly, Semi Annually, Annually |

|---|

Misreading Probabilities and Risk of Ruin

Monte Carlo often shows probabilities like:

- 10% chance of a 40% drawdown

- 2% chance of account ruin at a certain risk level

Don’t ignore small percentages. A 5–10% chance of ruin is huge in trading. Your goal is to push that probability as close to zero as possible.

Recommended Tools and Resources for Monte Carlo Testing

Standalone Monte Carlo Software

Several trading analytics platforms support Monte Carlo testing and can import MT4 trade lists. When comparing tools, check for:

- Flexibility in randomization options

- Clear charts and probability distributions

- Support for portfolio-level testing

You can also explore generic statistical or simulation software if you’re comfortable with data handling.

MT4 Plugins, Scripts, and Alternatives

There are tools and add-ons that connect directly or indirectly with MT4:

- Trade analyzers that import MT4 statements

- Strategy optimization tools with Monte Carlo modules

- Alternative platforms (like some professional strategy testers) that can run Monte Carlo on imported strategies

Also, learning more about MQL4 itself can help you design more robust robots. The official MQL4 documentation is a useful external resource for that purpose.

Learning Resources to Deepen Your Knowledge

To deepen your understanding of risk, expectancy, and system testing, you can study topics like:

- Probability and statistics for traders

- Position sizing and risk-of-ruin models

- System development and robustness testing

Educational sites on trading system design and quantitative methods are especially helpful. (For example, widely known finance education platforms explain Monte Carlo methods in simple language.)

FAQs About monte carlo simulations for mt4 robots

1. Do I need advanced math skills to use Monte Carlo simulations?

No. Most tools handle the math for you. You mainly need to understand what is being randomized and how to read the results—like ranges of drawdown, profit, and win rate.

2. How many trades do I need before running Monte Carlo on my EA?

More trades give more reliable results. As a rough guide, try to have at least 200–300 trades from a backtest or sample. For high-frequency systems, thousands of trades are even better.

3. Can Monte Carlo guarantee my MT4 robot will be profitable?

No. Monte Carlo doesn’t guarantee profits. It helps estimate risk and robustness. It shows how your system might behave under different random conditions, but markets can always surprise you.

4. How often should I re-run Monte Carlo simulations?

It’s wise to re-run simulations when:

- You significantly change your EA parameters

- You add a lot of new trade data

- Market conditions shift (e.g., volatility spikes or drops)

This keeps your risk picture up to date.

5. What’s the difference between optimization and Monte Carlo testing?

Optimization tries to find the best parameters for past data. Monte Carlo testing tries to see how those parameters behave under random variation and uncertainty. Together, they help you avoid curve-fitting and check robustness.

6. Can I use Monte Carlo on multiple EAs at once?

Yes. Some tools let you combine trade histories from several robots and test the portfolio as a whole. This helps you see how different strategies interact and affect overall drawdown.

7. Is Monte Carlo useful for discretionary (manual) trading too?

It can be, but it’s harder. You’d need a consistent record of your trades. If your rules are stable and repeatable, you can still use Monte Carlo on your own trade history.

Conclusion: Turning Data into Confidence With Monte Carlo Testing

Using monte carlo simulations for mt4 robots is one of the most effective ways to move from “hope-based” trading to data-driven confidence. Instead of trusting a single perfect backtest, you explore hundreds or thousands of possible futures and see how your robot stands up to randomness, slippage, and bad luck.

When you understand the range of outcomes—good, bad, and ugly—you can:

- Choose safer position sizes

- Set realistic expectations

- Decide when an EA is truly robust enough for live trading

Monte Carlo isn’t about eliminating risk. It’s about knowing your risk and being prepared. Combine solid strategy design, quality MT4 backtests, and thoughtful Monte Carlo analysis, and you’ll be miles ahead of traders who only look at one shiny equity curve.

Most Popular Forex EA

Onix Stratos XAUUSD EA: AI Smart Scalper for MT5

In stock

$0.00 $999.99Price range: $0.00 through $999.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $399.99Price range: $0.00 through $399.99

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

Zenith Matrix XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $899.99Price range: $0.00 through $899.99

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

In stock

$0.00 $797.99Price range: $0.00 through $797.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

In stock

Original price was: $109.99.$87.99Current price is: $87.99.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99

Gold Forex EA

Gold Forex EA