How to Calculate Sortino Ratio for Forex EAs: 7 Powerful Steps to Improve Trading Performance

Understanding the Sortino Ratio in Forex Trading

The Sortino Ratio is a powerful risk-adjusted performance metric used by traders to evaluate how effectively a Forex Expert Advisor (EA) generates returns while minimizing downside risk. When you’re running automated trading systems, stability and risk management matter just as much as profitability. That’s exactly where the Sortino Ratio shines.

Unlike other performance ratios that treat all volatility the same, the Sortino Ratio focuses only on negative volatility. Why? Because traders care more about losses than gains. This makes it especially useful for evaluating Forex EAs, which often run continuously and must be judged on consistent results.

The Sortino Ratio helps you answer one critical question:

Is your EA generating returns efficiently without exposing you to unnecessary downside risk?

Why the Sortino Ratio Matters for Forex EAs

Forex EAs tend to produce long sequences of trades. Some systems win often but lose big. Others win rarely but generate steady profit. The Sortino Ratio cuts through the noise and reveals how well the EA compensates you for the risk it takes.

A higher Sortino Ratio suggests:

- More consistent returns

- Fewer large drawdowns

- Better downside protection

- Higher-quality trade logic

Simply put, it’s one of the best ways to judge whether an EA is safe and reliable.

Sortino Ratio vs Sharpe Ratio

Many traders confuse these two. While both measure risk-adjusted performance, they’re very different.

| Metric | Measures | Weakness |

|---|---|---|

| Sharpe Ratio | Total volatility (up + down) | Penalizes profitable volatility |

| Sortino Ratio | Only downside volatility | More realistic for EA performance |

For Forex robots, the Sortino Ratio gives a far more accurate picture because automated systems often produce frequent small swings that shouldn’t be penalized.

Components Needed to Calculate the Sortino Ratio

Before you learn how to calculate sortino ratio for forex EAs, you must understand the components involved.

The formula:

Sortino Ratio = (Return – MAR) / Downside Deviation

Where:

- Return = Average return of the EA

- MAR = Minimum Acceptable Return

- Downside Deviation = Standard deviation of negative returns

These elements work together to show how well the EA performs relative to downside risk.

What Is Expected Return for a Forex EA?

This usually refers to the EA’s average monthly return or annualized return. You may calculate it using:

- Backtesting data

- Forward testing

- Live trading history

Higher returns improve the Sortino Ratio — but only if downside risk stays low.

Identifying the Minimum Acceptable Return (MAR)

Traders often choose:

- 0% (break-even return)

- Risk-free rate (e.g., treasury rate)

- Custom benchmark (e.g., 2% monthly target)

Choosing a more realistic MAR gives you a more meaningful Sortino value.

Measuring Downside Deviation

Downside deviation measures only losses that fall below your MAR.

Steps:

- Identify all periods where the return < MAR.

- Subtract MAR from each of those returns.

- Square the results.

- Compute the average of those squares.

- Take the square root.

This gives you true downside risk.

How to Calculate Sortino Ratio for Forex EAs (Step-by-Step)

This section explains exactly how to calculate sortino ratio for forex EAs using clear, simple steps.

Step 1 – Gather Historical EA Returns

You can pull:

- Daily returns

- Weekly returns

- Monthly returns

More data = more accurate results.

Step 2 – Identify Returns Below MAR

Filter out all returns above MAR.

Step 3 – Calculate Downside Deviation

Use the formula described earlier.

Step 4 – Apply the Sortino Formula

Insert your values:

Sortino Ratio = (Average Return – MAR) / Downside Deviation

A higher ratio means better risk-adjusted performance.

Practical Example: Calculating Sortino Ratio for Forex EAs

Let’s say:

- Average return: 3% monthly

- MAR: 1% monthly

- Downside deviation: 2%

Then:

Sortino = (3 – 1) / 2 = 1.0

A Sortino Ratio of 1.0 is considered solid for Forex robots.

Interpreting Sortino Ratio Results for Automated FX Systems

Here’s how professionals interpret values:

| Sortino Ratio | Meaning |

|---|---|

| > 2.0 | Exceptional EA |

| 1.0 – 2.0 | Strong performance |

| 0.5 – 1.0 | Average EA |

| < 0.5 | High downside risk |

Values above 2.0 usually signal an extremely stable EA.

Common Mistakes Traders Make

- Using too little data

- Ignoring MAR

- Mixing timeframes

- Confusing Sortino with Sharpe

- Not annualizing returns consistently

Avoiding these mistakes improves accuracy.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99| Validity | Monthly, Quarterly, Semi Annually, Annually |

|---|

Tools and Software That Calculate Sortino Ratio Automatically

MetaTrader Add-ons

Many MT4/MT5 indicators compute Sortino ratios automatically during backtests.

Professional Tools

Platforms like:

- Myfxbook

- QuantAnalyzer

- StrategyQuant

offer professional-grade Sortino Ratio reports.

(Example external link: https://www.myfxbook.com)

FAQs: How to Calculate Sortino Ratio for Forex EAs

1. What does the Sortino Ratio tell me about my EA?

It measures how well your EA generates returns while controlling downside risk.

2. What is a good Sortino Ratio for Forex EAs?

A value above 1.0 is good, and above 2.0 is excellent.

3. Does the Sortino Ratio work for scalping robots?

Yes — it’s even more accurate for scalpers because it doesn’t penalize upside volatility.

4. How much data do I need?

At least 6–12 months of returns, but more is always better.

5. Should I use daily or monthly returns?

Choose one and stick to it. Monthly data is the most common.

6. Can a high Sortino Ratio guarantee EA success?

No, but it strongly suggests the EA is stable and risk-efficient.

Conclusion

Learning how to calculate sortino ratio for forex EAs gives you a major edge in evaluating automated trading systems. It cuts through volatility, highlights true downside risk, and helps identify the most stable and reliable Forex robots. Whether you’re optimizing your own EA or selecting one to purchase, the Sortino Ratio remains one of the best tools for professional analysis.

Most Popular Forex EA

Onix Stratos XAUUSD EA: AI Smart Scalper for MT5

In stock

$0.00 $999.99Price range: $0.00 through $999.99

Elysium Vortex EURCAD EA: AI EURCAD Scalper for MT5

In stock

$0.00 $199.99Price range: $0.00 through $199.99

Equinox Cosmos GBPJPY EA: AI GBPJPY Scalper for MT5

In stock

$0.00 $399.99Price range: $0.00 through $399.99

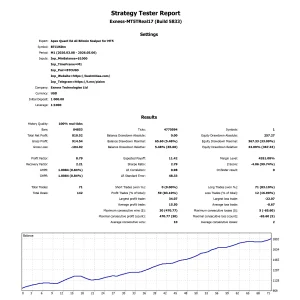

Apex Quant BTCUSD EA: AI Bitcoin Scalper for MT5

In stock

$0.00 $159.99Price range: $0.00 through $159.99

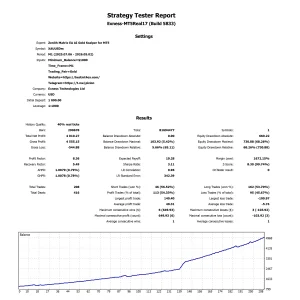

Zenith Matrix XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $899.99Price range: $0.00 through $899.99

Nexora Manus XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $699.99Price range: $0.00 through $699.99

Mythos Epic XAUUSD EA: AI Gold Scalper for MT5

In stock

$0.00 $849.99Price range: $0.00 through $849.99

Obsidian Aether EURUSD EA: AI Grid Scalper for MT5

In stock

$0.00 $797.99Price range: $0.00 through $797.99

AVA AIGPT5 XAUUSD EA: AI Gold Scalper for MT4

In stock

$0.00 $679.99Price range: $0.00 through $679.99

Golden Deer Holy Grail Indicator (Lifetime Premium)

In stock

Original price was: $109.99.$87.99Current price is: $87.99.

Powerful Forex VPS for MT4 & MT5 – Best Price

In stock

$44.99 $359.99Price range: $44.99 through $359.99

Gold Forex EA

Gold Forex EA